Bloomberg

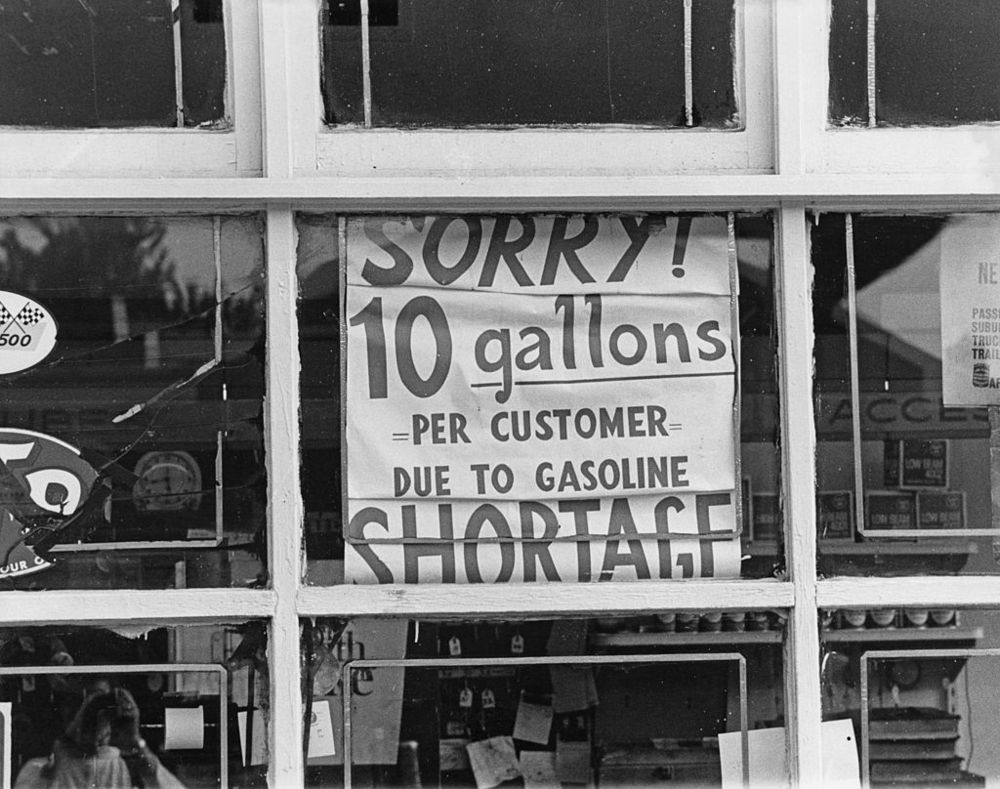

“The word for this is “stagflation” — we had a lot of it back during the 1970s. Shortages, supply chain disruptions, rising prices in an environment of unadmitted economic contraction — it’s a familiar landscape.”

“We’re in the opening stages of a major speculative bubble, and so people are investing in anything they think will gain in price. Cryptocurrencies are tailor-made for such a situation, as they can be manufactured freely and their only value is what someone else will pay for them, so they’re as popular now as investment-trust shares were in the runup to 1929.”

March 2021 post, John Michael Greer

Apologies for the extended delay in posting on the blog, it has been a very busy start to 2021! But I’m back with an update on where we are and this month’s post will focus on the economy.

Before I start, I thought it would be good to discuss the vaccine rollout which, so far, is going well with the vaccines apparently safe to the wider population.

As discussed in my earlier post, the question remains about the potential longer-term adverse side effects triggered by this mass vaccination rollout. Unfortunately, we don’t have enough data yet to know whether these risks are theoretical or real and, if so, how many people would be impacted.

I have tried looking into when you see serious long-term impacts, after a vaccine is rolled out, but it is not always clear. The Thalidomide scandal, where tens of thousands of children were left horribly deformed after pregnant mothers were given Contergan in the late 1950’s/early 1960’s took a few years to emerge. According to Wikipedia, the medication was authorised in 1958 but only withdrawn in 1961 in the United Kingdom, after birth defects were reported.

It is for this reason that pregnant mothers are generally excluded from vaccination programmes, given the potential risks to the unborn.

The 2009 swine flu vaccine – which I discussed in this post – was initially considered safe and approved for wider public use in September 2009. It looks like the first people to be vaccinated was in October/November 2009 but it was only in August 2010 that the European Medical Agency suspended the use of Pandemrix, given the reported triggering of narcolepsy.

So, to summarise, it took approximately 9 months before a vaccine that was given to 30 million Europeans was withdrawn due to safety concerns. Given that most of these vaccines have only been given since December/January 2021, a 9-month time-frame would mean any serious late side effects might become apparent by September 2021.

I have also read that scientists find the first 2 months of a mass vaccination rollout as the most critical, as it is likely that any serious side effects would be reported within those crucial 8 weeks. You can also argue, as John Greer does, that the Moderna and Pfizer vaccines are a revolutionary type of vaccine – mRNA – that we don’t have a track record unlike the more “traditional” vaccines like AstraZeneca/Oxford vaccine.

Ultimately it is the individual’s choice on whether they wish and indeed when, they choose to take a vaccine.

Moving on from vaccines, let’s discuss the state of the global economy.

The global economy contracted in 2020 and economists are predicting some kind of economic recovery this year, on the back of a fading virus and vaccination programmes. This doesn’t get us back to February 2020, economically speaking for the majority of countries, and it is likely to take years to get back to that 2020 peak according to the economist models.

I would argue that we will never, globally, return to that peak in economic condition and any recovery – which I’m sure there will be – will only partially take us back to a pre-pandemic level. Or, to put in more bluntly, we are now on the other side of the Long Descent, past the peak, and now in an era of economic contraction.

I agree with John Greer, who has recently written on his blog that the world is now entering into an era of stagflation; rising energy prices functioning as a tax on all economic activity, and drove the seeming paradox of inflation concurrent with high unemployment.

My parents, who were young professionals in the 70’s, remember fondly the days of high inflation and interest rates. They were able to acquire properties in London, and with their secure jobs, benefited from rising prices and inflation eating away at the real value of their mortgage debt. After the 70’s, the housing market boomed even further and they were able to trade up the housing ladder into the 4-bedroom house they own now.

For those with secure incomes stagflation can be a good decade, as my parents can testify. But for those who suffered from mass unemployment and relied on state benefits, I can imagine that the era of high inflation was grim and difficult. So be wary of taking on excessive personal debt in the years to come as it may come back to bite you.

In 2019, in one of my posts discussing the eventual economic Dark Ages, I made a series of recommendations on how to navigate these times.

I would still go along with this advice but would be more specific about equity allocation. In real terms, the stock market in the 70’s did badly as galloping inflation crushed the real value of stock portfolios.

The sectors of the stock market that did well during that decade were defensive stocks like utilities, healthcare and infrastructure along with commodities and gold miners. This article here goes into further detail the pros and cons of various stagflation investment plays.

A sensible portfolio would probably have a focus on healthcare, blue-chip defensive stocks and quality commodity resource companies.

The other hard asset that usually does well in these times is arable farming land and properties in quality locations.

Those Americans that brought discounted properties in California during the 1970’s would be laughing now, given the sky-rocketing rise in value properties over the last fifty years. The key is to buy properties in places that are likely to grow in real terms in the coming decades, something easier said than done.

I also agree with John Greer that crypto-currencies are in the early stages of a speculative bubble that is likely to inflate further as the Biden stimulus cheques start arriving in millions of Americans accounts in the coming months. A small number of cryptos are quality tokens with huge long-term potential, but there is no denying that it is a highly volatile asset class that tends to go through cyclical bulls and busts. Right now, we are in a bull cycle, that is likely to carry on for a while longer, but at some point, it will reach that manic phase, after which the bubble will burst.

For those readers, like me, who are invested in this exciting if highly speculative market, I suggest that once you sense that we heading into the late stages of a bubble, to sell and get out and invest the profits into something I have suggested in that list above (not crypto!).

Overall, my thesis remains that we are broadly tracking the Limits to Growth megatrend, and we peaked in global economic activity in 2020.

2021 will be a story, like most years going forward, of economic contraction amid a broader macro environment of supply chain disruptions, geopolitical tensions and rising prices. The crypto and stock markets are enjoying the “sweet spot” of the central bank money printing bonanza, but the party can’t go on forever.

I expect that the Biden stimulus cheques, along with a re-opening of the US economy, will drive a mini-economic boom in 2021. The optimism generated by this will drive the stock market (and crypto market) into mania territory towards the latter end this year.

If I am correct, this is likely to be a good time to crystalise profits, get out and ensure that you have a comfortable safety net as the stagflationary forces of higher prices, interest rates and mass unemployment come down the road.