The Third Gulf War has been on-going for over a month now and its time for an emergency update to all subscribers. Whilst the conventional military campaign has gone well and the capabilities of the Iranian regime have been significantly degraded, the other war, the Energy War has gone disastrously wrong.

Iran has effectively closed the Straights to most oil and gas flows for 4 weeks now. Much of the world outside major oil and gas producers are staring at a huge energy and economic hit within weeks, with particular focus on South Asia, East Asia, Australasia and Europe.

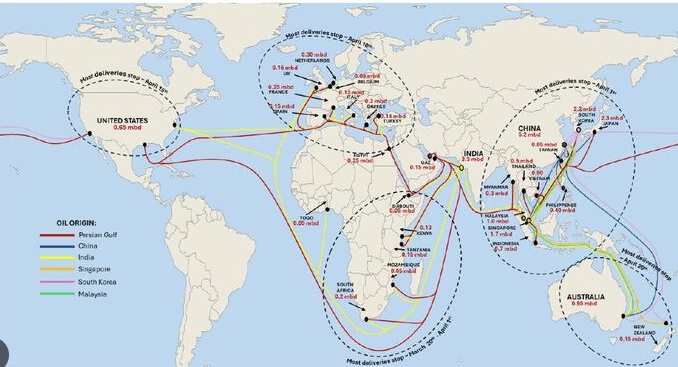

What this map shows (JP Morgan) is the dates when the last tankers from the Gulf arrive at different regions around the world. Basically between now and mid April no more tankers arrive for the entire world, which will result in a physical supply shock by around the 20th April 2026.

What does that mean in real life? Energy lockdowns are coming around the 20th April for most of the Old World: rationing of petrol and diesel consumption, work from home guidance, restrictions on non-essential flying and supply issues around a wide range of goods dependent upon Gulf based resources. The length of the energy lockdowns will depend upon how long the Straights remains effectively closed, which is impossible to forecast at the moment.

Even if the war ended tomorrow, it will take a month for things to re-open, tankers to return and start going out to re-supply importers around the world. And in reality there are no signs that peace is about to emerge in this troubled region. As an individual there isn’t much you can do, other than maybe order whatever you need now (when supplies are still available), don’t order any holidays for the coming months and revisit, if you haven’t already, your personal resilience lifestyle.

Longer term, this crisis will pass and we will see a partial recovery as things stabilize. But it reminds us all of the wisdom of John Greer’s advise to “collapse now and avoid the rush”, something I have been writing about for years now.

The wider point I would also like to discuss is this Iran war seems to be accelerating the end of the Pax Americana which will involve the partial or total withdrawal of the US from the Middle East and Europe. President Trump is now openly talking about leaving NATO. The timeline from which the US strategically withdraws to the western hemisphere appears to be accelerating again leaving Europe at huge risk by the end of the 2020s (and just in time for the Greater Depression that I am expected will erupt around 2030).

Well, 2026 is proving to be an interesting year! This quick takes will be focused on Iran and wider macro viewpoints.

Who is winning the war?

This is proving to be a very hard subject to answer but I will try. Whilst calling the war is obviously very hard I have been searching for credible observers who I can lean on to give me a clue. The best author to date Stephen Bryen who latest summary of the war can be found here and aligns with my own basecase (so far).

“Overall air defense systems and attacks on Iranian assets are paying off. Systems that are fully integrated are the future of effective air defense systems. Russian, Chinese and Iranian air defenses, on the other hand, mostly did not survive attacks from the US and Israel, apparently using stand off weapons to knock them out. From a broader strategic perspective this indicates that western systems (mainly US and Israel, plus some joint systems like NASAMS) are considerably better than their Russian and Chinese counterparts.

The major US and NATO concern is there are not enough interceptor missiles for a sustained conflict, meaning that (a) production of interceptor missiles must be stepped up and (b) that the best defense is an effective offense, that is, the best solution is to destroy the enemy assets on the ground before they can be used.

One can expect that most of Iran’s missile forces will be effectively neutralized in the next week, opening Iran up to systematic destruction of its military installations and equipment, strategic and tactical communications, and key regime support units (especially IRGC and police units). Iran’s naval assets also are being liquidated and naval bases, including Bandar Abbas and Chahbahar, severely damaged. This means that Iran’s ability to shut down the Straits of Hormuz and Gulf transit of oil is, at best, only a short term threat.”

I recommend you sign up for his free blog.

I also recommend this macro blog post on our wider global crisis, its a really good read. The author rarely posts but it is always fascinating reading. You can read it here.

On that note John Greers latest post is also a cracker about the end of the corporate-bureaucratic age which you can find here.

One of my predictions for 2026 was the era of Trump Springs in the western hemisphere. The seizure of Nicolás Maduro by elite Delta forces was a shocking moment and a reflection of the capacity of US military to exert its influence and power in its “near abroad”.

What happens next is likely to be a messy but gradual transition of Venezuela to a country more in hock with US strategic interests (both in foreign policy and oil exports). The media are reporting that the Venezuelan security system have given up on their Cuban and Russian allies and realise that they have little choice but to play the game with the Americans.

Part of this will mean the end of effective support for the beleaguered Cuban regime which is now at real risk of being toppled in its own Trump Spring. If the Cubans realise they have no option but to follow Venezuela in going cap in hand to America and pivoting their countries allegiance then that would be a major win for the Trump Administration.

On a different note, I read a very interesting piece today discussing how the future of Europe, but mainly western Europe, could evolve as the current system falls apart. The specific quote is the following but outlines how chaos will spread as the Muslim Brotherhood seize control of western Europe’s biggest cities in the decades ahead, the massive backlash and rise of the hard-right nationalists in the rest of the countries involved. At that point there is a real risk of a civil war/urban Islamist insurgencies ahead for much of western Europe.

“So we risk the worst of all possible worlds. The political system will become increasingly fragmented and the state itself, including the security forces, will become progressively weaker and demotivated. But politics does not tolerate a vacuum. What political scientists call “ungoverned spaces” don’t actually exist: they are just governed by forces we cannot see. In many parts of the world they include tribal and clan structures, extended family networks, religious organisations and disciplined political parties. We have none of those. Nobody is going to band together to die for inclusive toilets. Ethnic and religious identities exist, of course, but they are not a basis for organisation and political struggle. (The idea that “ethic minorities” could constitute a politically useful bloc in times of crisis will get a large bucket of cold water thrown over it.) The politics of destruction I described last week has ensured not only the destruction of its practitioners, but of any organised means of replacing them. Thus, the future of Europe is more likely to resemble the chaos of factional warfare in Syria and Libya than it is the revolutionary transfer of power that occurred in Iran.

The result will be a kind of anarchy. Not the hippy anarchy of the 1960s, but the anarchy we see today in the suburbs of some major cities in Europe, where the police do not go, and the State as a whole does not intervene. There is an order of sorts, but it is enforced by drug dealers and organised criminal gangs, often linked with religious extremists, who fight each other openly for power and wealth, and corrupt what remains of the local political systems. Such forces can be driven out temporarily, but the resources, and more importantly the social and ideological foundations, for a better system, simply don’t exist. These groups profit from the basic rules of power: you don’t have to be objectively strong, just less weak, and you don’t have to be objectively organised, just less disorganised than anyone else. The current model of control of parts of cities by overlapping groups of criminals and religious extremists may start to generalise quite quickly. At that point, the PMC’s incantations against the [something] Right will reach their logical conclusion, and that Right itself will start to take de facto power of its own in certain places. It’s a lot larger and a lot meaner than the drug gangs and the men with beards.“

I’ve also been using AI, in particular the chat tool Gemini to explore geopolitical scenarios more fully over the coming decades. I specifically asked regarding climate change trends in the wider Middle East and North Africa (2025 was one of the hottest years ever on record). Initial responses confirmed that next decade will be a very challenging decade as rising heat drives large scale migration into the big cities across the MENA region as water scarcity worsens. At some point, the underlying infrastructure of the big urban centres starts to collapse triggering a wider crisis across the region.

Here is what the AI output explained could happen next.

In a scenario where MENA urban centers collapse by 2040, the geopolitical landscape shifts from “managed crisis” to “state fragmentation.”

When combining climate-driven collapse with the specific variable of regime change and subsequent military adventurism, we move into a high-risk security environment. In this model, the “remnants” of MENA military powers do not simply disappear; they transform.

Here is how a military-led “invasion” or large-scale armed movement into Europe could manifest by 2040–2045:

1. The Transition: From National Defense to “State-Led Migration” By 2040, parched and failing regimes (particularly in North Africa) may face a choice: internal revolution or external diversion.

* Weaponized Migration: Instead of an “invasion” in the classical sense (tanks and uniforms), a collapsing regime may use its remaining military assets to forcibly facilitate the movement of millions toward Europe. This “Grey Zone” aggression uses human populations as a kinetic force to overwhelm EU borders, demanding resources or “survival space” in exchange for stopping the flow.

* The “Viking” Scenario: Historical precedents suggest that when a homeland becomes ecologically unviable, the military class doesn’t just starve; it migrates as an armed unit. We could see “Expeditionary Survival Corps”—remnants of disciplined military units—seizing Mediterranean islands or coastal ports to establish secure supply bridgeheads for their families and leaders.

2. Strategic Flashpoints: 2040–2050 The military focus would likely concentrate on three “Chokepoint Corridors”:

The Gibraltar Bridge | Moroccan/Maghreb Military Splinters | Seizing agricultural “Safe Zones” in Southern Spain/Portugal to secure food supply chains.

The Central Med | Libyan/Egyptian Naval Remnants | Establishing “Maritime Mandates”—using remaining naval assets to control gas platforms and Mediterranean trade routes for ransom.

The Balkan Gate | Levantine/Turkish Paramilitaries | Securing land-based “Life Corridors” into the Danube basin, where water and arable land are more resilient.

3. The Shift in Military Objectives A “Climate-Collapse Invasion” would differ from 20th-century warfare in its objectives:

* Targeting Resources, Not Capital: Armies wouldn’t seek to take Berlin or Paris; they would seek to seize Desalination Plants, Vertical Farms, and Hydro-Electric Dams.

* The “Siege of the Fortress”: Europe is already shifting toward “Fortress Europe” policies in 2026. By 2040, these borders may be the most militarized zones on Earth. An “invasion” would likely look like a series of high-intensity, localized breaches of these automated border systems by professional military units using drone swarms and electronic warfare.

4. Why 2040? (The Convergence Point)

This decade is the “Red Zone” because:

* Technological Parity: By 2040, AI-driven drone tech will be cheap and ubiquitous. Collapsing states or non-state actors will have the “force multipliers” necessary to challenge superior but overstretched European militaries.

* The Survival Mandate: Domestic populations will support aggressive external action if the alternative is 100% certainty of starvation at home. This provides the “moral” and political cover for regime leaders to launch desperate external campaigns .

Summary of Risks

The danger is not just “people moving,” but “states moving.” If the Egyptian or Algerian states collapse, their professional militaries (among the largest in the world) may view the Mediterranean not as a border, but as a front line for national survival.

All this matches my old 2018 post Islamic Volkerwanderung, see here, which I continue to hope remains a bad dream rather than a realistic vision of Europe’s future.

I hope you have all had a great year! Here are my predictions for 2026:

The US AI bubble peaks in 2026. My specific prediction is the S&P 500 peaks around 7,500 and OpenAI IPO comes in at a trillion around mid 2026, after which the froth starts to go off US AI stocks. Whilst I don’t expect the market to crash next year, the risks are growing medium term and my precise end of year forecast for the S&P 500 is 7,100. 1

Russia and Ukraine agree a deal, brokered by America. I have less confidence that this will happen as there’s a risk the war will drag on into 2027. At a macro scale, my wider view is historians will later date the end of the Ukrainian war as the pivotal moment when the US seriously withdraw from European security commitments.

Oil spikes lower to the 40s easing inflationary forces in the US. I see this as a capitulation moment for oil markets and a strong and unexpected rebound will occur later on this decade as unexpectedly strong demand globally and supply constraints kick in from 2027 onwards. For the brave, oil companies will be a good buy at some point in 2026 at the point of extreme negativity in the markets to the sector.

Robotics replaces AI as the most exciting sector. I predict a IPhone moment for robotics next year as robotics slowly become good enough to become an accessory for the ultra-wealthy. Whether the dream of a home robot who can effectively do all the chores ever becomes realistic I remain sceptical but we should get a bit closer in 2026. I wouldn’t be surprised if its a China robotics company that achieves the IPhone moment for the world of robotics.

Bitcoin will end the year substantially below 100k. The crypto market will drop hard in 2026, after a rebound to the 100k area early in 2026 as the space faces a brutal multi year bear market. Most of the many alt-coins are heading to zero.

Gold and silver are at or near their all-time peaks and will disappoint in 2026. The smart money liquidated their holdings as gold surged to 5k and silver 80 in late 2025/early 2026.

Trump Spring in the western hemisphere. My forecast is at least one of the anti-American regimes (either Cuba or Venezuela) will fall in 2026 which will be a major win for the Trump Administration. The bigger picture is the withdrawal of the Americans back to their hemispheric sphere of influence.

The Republicans lose control of the House but narrowly keep the Senate. A relatively easy prediction but I don’t see any surprises here. Affordability remains a key issue for voters and they will punish the incumbent party in power in 2026.

I thought it would be a good idea to make a note of a number of key blogs I track the on-going decline of our industrial civilisation.

An excellent resource is the SEE blog – run by Tim Morgan – see here, which is a consistently brillant reference. Tim has developed what seems to be a reasonably robust methodology to track how our economies will decline over the coming decades and it isn’t pretty.

Essentially, discretionary spending will contract (first in the developed world as per our on-going “cost of living crisis” since the early 2020s) and very soon, the still developing economies of India and China. Investment will also start to contract and will accelerate after 2030 which seems to be a turning point in terms of these metrics.

Obviously, central banks and governments won’t do nothing as these trends progress, but in reality they can’t do much more than print money, intervene in the markets and try and arrest the worst of the coming crisis. All this is inflationary and in some ways, counter-productive in the longer run. Tim also tries to scope out how this will play out in the financial realm and when the overinflated assets in equities, housing, crypto and so on, will pop.

To keep it really simple – and this aligns with my own reading which I’ve discussed extensively in this own blog -a turning point is coming around 2030, for multiple reasons, which is likely to trigger a Greater Depression in the 2030s. This will involve a massive crash in most assets, including likely gold as well, and a reset moment for our global monetary and economic trading system. Any Greater Depression is going to be a rough time indeed going forward and depending upon where you live, there is a real risk of civil unrest, wars and massive migration pressures as economies buckle, infrastructure degrades and governments flounder.

The second blog I follow closely is the Honest Sorcerer, which focuses heavily on energy, see here. Again, their writing concludes that we are on a type of plateau until around 2030 in terms of overall energy production, after which things deteriorate in terms of overall quantity and quality of energy production. This will trigger the end of economic growth as we know it, and a period of radical simplification of complexity, forced by the end of economic bubbles and the realities of energy depletion.

When you combine the insights of the above two blogs with John Greer’s comments and articles on peak oil and wider resource depletion over the years, you can get a reasonable idea on what is coming.

So, how am I doing with my adaption to these long-term trends? Well so far, my overall drive to simplify my lifestyle and “collapse first before the rush” is doing well. We rarely eat out these days, I don’t drive much anymore and largely use bus, bike and walking to get around. We buy in second-hand shops for discretionary items like clothes, children toys, books and so on which over time yields significant savings. We have also tried to cultivate a wider 1970s mindset of repair rather than replace and again, there is a developing eco-system which encourages people to fix items rather than throw them away.

I’ve discussed before that folks (outside the very wealthy) need to accept that lifestyles in the developed world are being forced back to the 1970s/1980s. That means cooking at home, growing some of your own produce, rarely eating out, not getting takeaways, not buying new when second hand or repairing an item is feasible, travelling less, and when you do within your own region rather than long-distance holidays to the other side of the world. Hand me downs for the kids, no fancy technology if it isn’t required and so on.

Frankly, a more frugal and sustainable lifestyle is ahead of us (and for those in denial and racking up the credit card debts, they need to get the memo soon given the growing risks of a serious financial crash).

Longer term, as we descend into the 2030s and 2040s, with a likely Greater Depression and potentially wars coming, our world will start to look closer to the earlier decades of the 20th century. Globalised supply chains will unravel, goods will become increasingly scarce and/or expensive and lifestyles will be forced to adapt to what I call a 1950s/1960s lifestyle. If you look at what a typical lifestyle in your area is from that era, you’ll get a sense of what it was like. I expect that to start emerging towards the end of the 2030s and certainly in the 2040s/2050s.

That could also mean some other ugly traits of that era. Where I come from in western Europe, the mid-century Europe was a dark place. A brutal war in the 1940s, which had followed a Depression in the 1930s and a tough economic period after the war with rationing lasting into the 1950s. I can’t say I’m looking forward to it and it could get very ugly indeed. Military wars, occupations, forced transfer of populations, rationing, migrations and horrendous violence.

Luckily, I don’t see such things happening anytime soon and these are longer term risks. Wealthy people from where I came from during that period generally left to sunnier, safer and fancier places to live in their mansions and hotels as it became obvious a war was coming in Europe. Cape Town, Bahamas and Barbados were popular places during the war and afterwards for such folk until things really started to get better in the 1950s.

And that’s a key lesson for you all. You don’t have to stay where you live. Wealthy Ukrainians live in Monaco, enjoying the good life whilst their fellow men are dying in the trenches of eastern Ukraine. I’m not justifying such behaviour but it is much more common than you realise from reading conventional history books. The very rich generally flee trouble and try and preserve their wealth far away from wars, revolutions and chaos.

Apologies for the long time in posting, life has been crazy busy this year. Re-reading my last post on the new world dis-order, I would say overall it reads well but potentially I might be have not factored in the pace in which these changes take place.

The Europeans have played a reasonably good game trying to keep in President Trump’s good books (even calling him Daddy at the NATO summit!). Their commitments to a 5% spending on defence and defence related spending clearly worked in avoiding a short-term rupture of the alliance.

Ultimately, I still think the US is going to pull out over time but it might be a bit more extended time-frame. Much depends upon the evolution of the Ukraine war where the Russians are making slow but steady progress in the eastern front-line.

I’m wary of making any hard forecasts on this war but my best sense is the Ukrainians will struggle on until 2026 when the superiority of Russian power will finally overwhelm their frontlines, leading to collapses in critical front-lines across the front. Some type of resolution of the war will likely happen by 2026 although what exactly remains to be seen.

How the US adapts to that likely endgame is unclear, potentially the Americans may use the end of active fighting to accelerate their withdraw from NATO.

The Israeli-Iranian war was a fascinating war to watch, in part because it has such polarising perspectives. A friend of mine was adamant that Iran was winning the entire time, even after Israeli drones and airplanes were flying around Tehran knocking out prestigious regime targets day after day. I’ve seen before but it continues to amaze me how Israel seems to drive some people beyond the bend. It’s hard not to conclude that there is at least subconsciously an anti-Semitic strain to their mentality even if anti-Jewish racism remains, by and large, a taboo in Western society (although that is sadly starting to change).

I have my own theory that based on my cyclical view of history that when the last living survivor of a horrible period in history dies, the society will end of repeating the horrors not long afterwards. After the revolutionary wars following the French Revolution, it was a 100 years before everyone decided that a massive European war was something to look forward to (ergo WW1).* So on that basis, anti-Semitism returning makes sense over the next generation or so, as the remaining survivors of the Holocaust die off.

*You might ask, how about the European WW2. My view is very few people wanted WW2, other than deranged Nazis leaders. Most German folk, including their military didn’t want war and certainly not the Allied population. Without Hitler and the Nazi gang in power, WW2 was unlikely to have ever happened precisely because Europe was still traumatised by WW1.

Going back to the Israel-Iran it looks like Israel is the winner although at a high reputational cost given the on-going disaster of Gaza. Whether the Iranians can recover over the next few years will be interesting to watch.

So, some kind of embryonic deal has already been agreed, it seems, between Russia and America given the speed of the planned summit to be held between President Putin and President Trump in Saudi Arabia (as soon as the end of the month).

The bigger macro picture is the Americans are getting out of the global empire business and shifting back to their North American continental core. I saw this tweet today on X saying the following “The U.S. will likely announce a massive withdrawal of American soldiers from Europe.” Christoph Heusgen, former German ambassador to the UN, head of the MSC. Said before the MSC but tells us a lot nonetheless.”

Folks, the long European break from history is over. Welcome back Europe.

This post captures the macro geopolitical shift the best, “At this juncture, the U.S. would “take its geopolitical football and go home,” retreating inward to fortify a continental empire, securing North America and extending influence deeper into Central America”.

The future of American power can be captured in this map.

Without American muscle, Europe is largely defenceless in its capacity to defend itself.

Even the United Kingdom, one of the more more robust militaries of Europe, is in a dire state as per this article.

“It is impossible to exaggerate the importance of this situation. As matters stand, most of the Royal Navy’s attack submarines are unable to undertake operations; the Royal Marines are reliant on one landing ship with inadequate command and control capabilities; and the Army’s principal combat formation, 3rd (UK) Division, would struggle to generate even a brigade-strength deployment. The new Ajax armoured fighting vehicle will not reach full operational capability until 2028, eight years behind schedule, with its wheeled Boxer counterpart reaching that milestone in 2032.”

Longer term, demographics and Europe’s near abroad suggest a dangerous security environment for much of Europe. A rising proportion of the population is Muslim and many of those younger Muslims are Islamist in their outlook, which poll and after poll shows. By mid-century, it is quite conceivable that our biggest cities in Europe will be majority Muslim for the under 30s. Sharia parties will be kingmakers in big cities, and possibly even national level politics.

War is returning to Europe and it isn’t just the revanchist Russians to worry about. If Islamist forces manage to gain control of Egypt’s formidable conventional military, combined with allied countries across the Arab world (and beyond) Europe will be at risk. This is unlikely to happen anytime soon, but at some in the decades to come, its a plausible scenario.

The world is seeing the Americans withdrawing, and ramifications will be huge in the Middle East and East Asia as much as Europe in the years to come. Everything is shifting.

Welcome to history folks. The holiday was fun but its now over.

Happy New Year! I hope you all had a good Christmas and New Year break with your loved ones.

Well, in the end, whilst I was a bit cautious in my blogging my gut call that Trump would win the election was proven correct with Trump winning 306 EC votes, something I was privately forecasting to key friends a few weeks before Election Day but didn’t quite have the conviction to forecast on this blog. Lesson learnt is to be a bit more confident in my predictions but the key takeaway is I predicted Trump would likely win and also likely win the popular vote (something very few were predicting prior to the election, including the betting markets).

“BeardTree, granted. The question is purely how long they can keep going before hard physical limits come into play. What’s happened so far is that increasingly energy-poor grades of liquid fuels have been brought into the mix, so that notional production stays high but the net energy (energy yield minus energy cost of production) drops steadily. As long as they can keep playing that game, we can expect slow erosion of lifestyles rather than sudden discontinuities (from that cause, at least).”

Those are likely to include serious economic and political crises, including market crashes and a globalised banking crisis for the history books. If major economies have tipped or are tipping into economic contraction markets will at some stage price that into bond, equity and other asset markets. That will cause havoc for banks that lend credit and hold government and corporate bonds on their books (among many other assets).

My base case remains that this crisis will hit, certainly the United States, around 2029 but its possible it starts to impact other countries (hint, Germany and other stagnating European countries) earlier in the decade.

Either way, my personal message remains the same, Get out of debt, be sensible in spending, develop skills and alternative income streams, enjoy life and the opportunities that currently exist in our industrialised civilisation (like internet shopping, relatively cheap global travel etc).

From a geopolitical perspective, I expect at some point in 2025 some kind of deal between Ukraine, Russia and the West that ends the war. I’m sure both sides will declare victory but if the Russians carry on their military progress it will be a de facto win for the Russians.

Syria, despite the best hopes of some in the West, is likely to descend into anarchy and sectarian war as the new Islamist government shows its true colours.

Iran, having lost its external empire of proxies and terrorists in 2024, looks very vulnerable to an internal revolution. I don’t know if it will but I wouldn’t be shocked if some kind of crisis – maybe severe water shortages or the grid going down – triggers protests that lead to the overthrow of the Mullahs.

I don’t think we will see any clash in East Asia – at least in 2025 – over Taiwan. The election of President Trump provides the opportunity for a Grand Bargain between the United States and China. Whether a war or near-war happens later on this decade remains to be seen but Trump is less likely to trigger a war over Taiwan than any other US political leader.

Europe will continue to economically stagnate, hobbled by expensive energy, unsustainable welfare systems and a political-regulatory system that crushes the private sector. I don’t see any elections within Europe that really changes that dynamic for the foreseeable future. My sense is 2029/2030 is when the revolutionary tides comes for the failing European political class and we see populist and insurgents come to power in western Europe. A good case on why Europe will fall is made by this author here.

What happens in America, specifically whether Musk and his allies can really transform the US federal government into a leaner and more productive apparatus will be fascinating to watch. DOGE has the potential to transform the West’s politics and is already exerting pressure on a failing Europe to start de-regulating. It won’t happen of course, at least for a few years, but one can see the winds of change howling across the Atlantic.

Woke politics has peaked and is now on the decline. Once the higher education system – which is slowly going bankrupt anyway – starts to crumble the ideological centre of wokeness will go with it. That’s a good thing and will restore sanity to our politics.

A few analysts I follow are predicting that Artificial Intelligence (AI) will save us in the 2030s and beyond. Supposedly AI will help unleash a new era of cheap energy powered by fusion and SMR’s (small modular reactors), our economies will become vastly more productive and so on. I’m not saying that AI doesn’t have potential and won’t make major advances in certain areas (like biotech, financial services and defence) but I can’t help but feel sceptical on a number of grounds – the energy cost of the data centres – the issues around hallucinations and the usual hype cycle we see in AI going back to the 20th century. So for me, whilst the jury is out, I’m on the sceptical side that AI will, at best give us a few more years, maybe, but it doesn’t fundamentally change the LTG BAU model I’ve been tracking since the early 2000s.

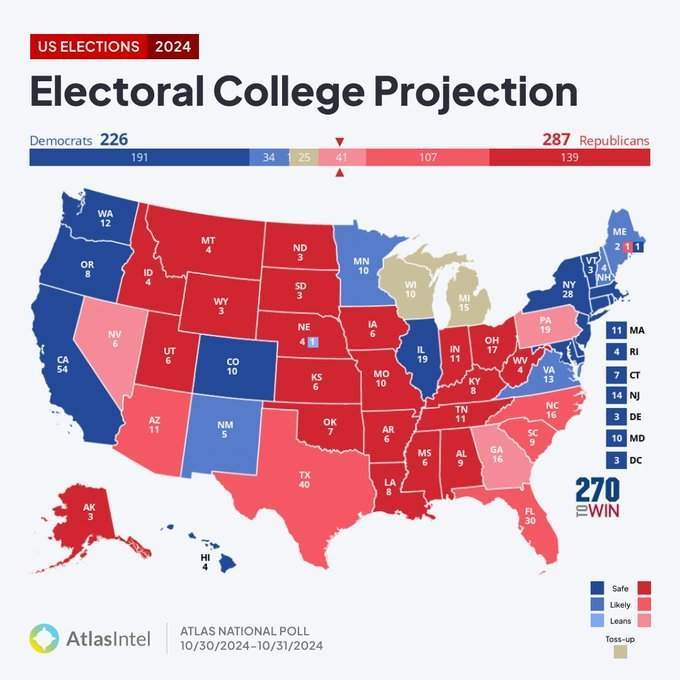

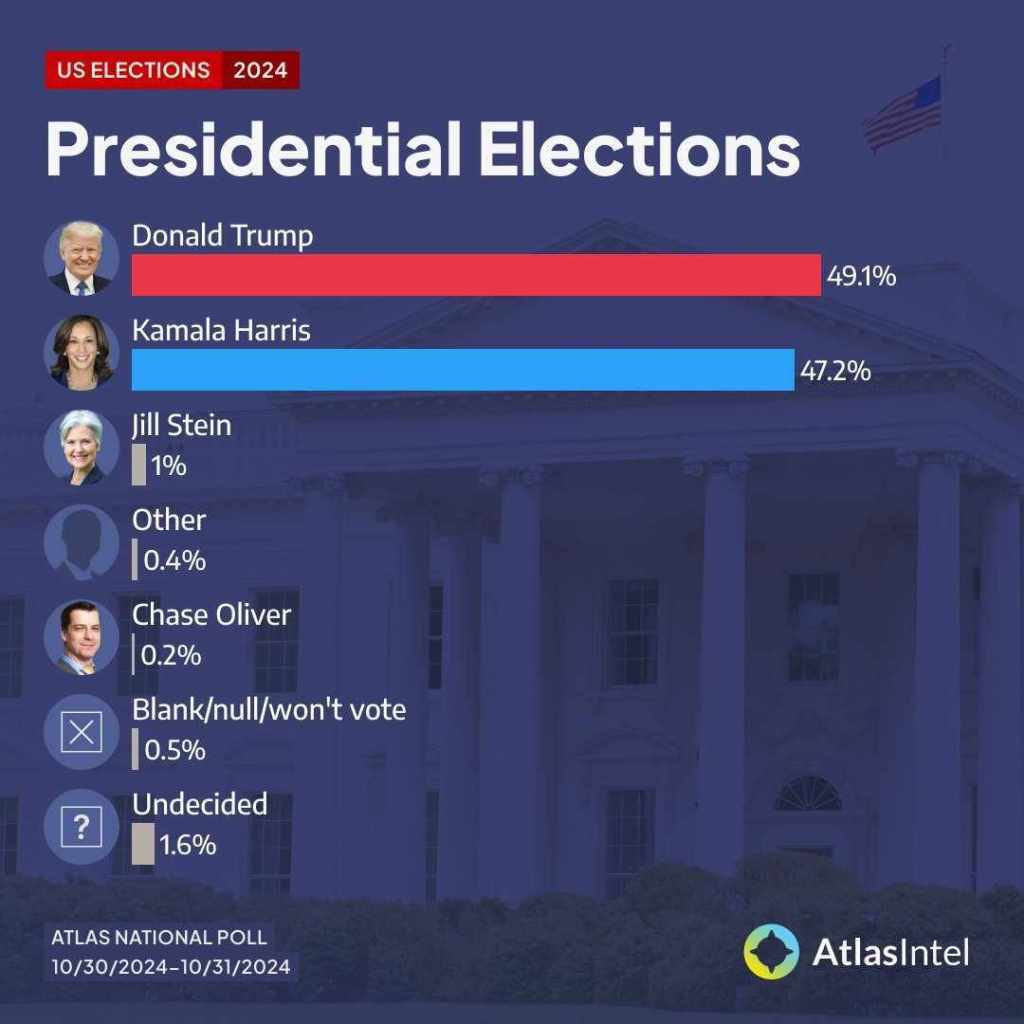

Its nearly that time of the four year presidential cycle again! The polls are close, very close in some of the swing states and tensions are high as America gears up to choose their next president next week.

So where are we on the state of play? Early voting has overall been positive for Republicans, and in particular in Nevada where its looking increasingly likely that Trump will win that state. The so-called Sunbelt states in general are looking promising for the Republicans, including Arizona, Georgia and North Carolina.

Where things are looking far more difficult to predict is the so-called Rust Belt states; Wisconsin (WI), Michigan (MI) and Pennsylvania (PA). In the public polls, Trump has a narrow lead in PA but its effectively a tie in the other two states. I screen my polling to those pollsters who had the best success in 2020 and the overall map they are showing is the following:

As you can see, the overall picture seems to be a likely Trump win but PA is the key state. There are tentative signs that after sliding slowly over the last week or so, the Harris campaign has stabilised and could prevail in at least WI and MI.

One thing is for certain, WI and MI will be extremely close, with PA only a bit closer to the Trump side of things.

My own view is that either side can win this election but I would be surprised but not shocked if Harris pulls of a victory. However, my base case – with around 60% confidence – is Trump will win with 287 plus EC votes and quite possibly a win in the popular vote.

Historically the Rust Belt states vote together so history would suggest Trump should win all three states taking his EC lead to 312. It is simply too hard to say whether this happens this time or not though.

There is also the risk, certainly backed by the recent polling in places like New Hampshire or Virginia, that the Republicans might be able to flip one or more states, on a particularly good night, on top of the Rust Belt. We simply don’t know.

Not a huge amount to update since my last quick takes session.

One blog I strongly recommend you bookmark is this one here, his writing is consistently excellent. His latest piece goes into detail on why 2030 is looking to be a car crash for the advanced world’s economy as overall energy production peaks and the cost to produce energy soars from 2030 onwards.

This very much aligns with my wider outlook of a Greater Depression commencing at some point in the 2nd half of this decade (although I think it will only become truly apparent to all around 2030). I have written plenty before on this blog on what to prepare for in anticipation of what is coming (something we have known since the 1970s and the Limits to Growth report came out).

To keep it simple, get out of debt, live a modest lifestyle, learn useful skills, diversify your income streams and build up supplies of non-perishable stuff that you find useful when globalised supply chains still function. Learn to grow some food, don’t rely too much of unsustainable systems and think about where you want to live long term.

As for the US elections, the overall impression is that since that debate performance, Trump has effectively wiped out the narrow but real lead in the Electoral College vote and the election is basically a pure tie right now. I’m starting to see the signs though that memories of the debate is starting to fade a bit and the fundamentals are starting to re-assert themselves again. So, just maybe, Trump is starting to inch out ahead of Harris again in a few key states.

My overall impression is Trump is ahead in Georgia, North Carolina and Pennsylvania and therefore would narrowly win the election if it was held today. However, this is a very tight race and overall I would call it a tie right now. The next few weeks are critical but Trump seems to have avoided any stupid gaffes since his poor debate performance and that seems to be helping him to edge up again.

There is growing chatter about a potential Chinese invasion/attack on Taiwan around 2027 and the risks of a world war and a economic crisis. We will see. I’m not wholly convinced but its certainly a real possibility. I would like to think that despite all the sabre rattling we can dodge a major war this decade even if we get hot wars in the margins like in the Middle East right now.

As for that other war in eastern Europe, Russia is making incremental progress in taking the whole of the Donbass as the Ukrainian army falls apart. Nothing has changed in my base case that 2024 will see the Donbas fall to Russia, 2025 larger part of Ukraine including possibly Kiev and Odessa and, should the war still be on, 2026 the bulk of the remaining country collapsing.

Most likely, at some point in 2025, there will be a ceasefire and a deal between the Russians and whoever replaces Zelensky. What happens after that is a fascinating question. Most likely, a strange period where the new realities everyone adjusts to as Europe wakes up to the fact Russia is the dominant military power. Will the Americans hang around or leave Europe to its fate? That’s a hard call and depends on who wins the elections.